The convenience of setting up a direct debit facility to pay your bills is always tempered by the difficulty and hassle of cancelling this method of payment when necessary, and it seems banks are failing in their duty to customers.

The Banking Code Compliance Committee (BCCC) has released a report suggesting that in around 29 per cent of cases banks fail to act in accordance with customer wishes when trying to cancel direct debit payments.

The BCCC conducted a mystery shopping exercise into banks’ compliance with their obligation to promptly cancel a customer’s direct debit on request and the results were a significant cause for concern, according to BCCC independent chair Ian Govey.

Read: ATO issues advice to surging numbers investing in shares

While the results were bad, last time the BCCC ran this exercise back in November 2018, there were 54 per cent of cases where banks had not processed direct debit cancellations in a timely fashion, suggesting some improvement in the industry.

The banking code of compliance stipulates that banks must promptly process a customer’s request to cancel a direct debit and must not ask or suggest that the customer first raise the cancellation request with the service provider.

These provisions are particularly important for bank customers who are experiencing financial difficulty and for whom direct control over their finances can mean the difference between food on that table or not.

Read: NAB slapped with $18.5m fine for misleading customers on fees

The most common mistakes, the report found, were staff members from banks telling customers that they should contact service providers to cancel a direct debit arrangement or that the bank could cancel the direct debit but the customer should contact the merchant first.

The report found that many staff members in banks did not understand the nuance between a direct debit and a recurring payment.

The BCCC has highlighted several initiatives to improve bank compliance in this area, including updating information on their websites, better staff training and communication programs, and additional monitoring activities.

Read: Pensioner’s plight highlights need for better bank behaviour

Consumer Action Law Centre chief Gerard Brody told The New Daily that the BCCC report is further evidence that banks are falling short of their promises to Australians.

“There has been a history of really poor compliance,” he said. “This provision is really important: it gives people control over their own finances.”

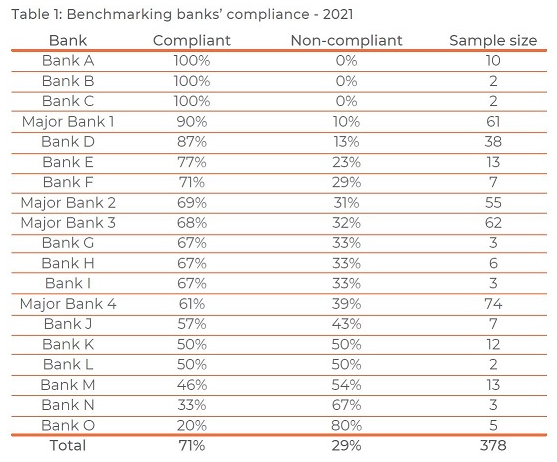

The BCCC report does not name the individual banks but it does separate out the performance of the big four banks, with one in particular recoding 39 per cent non-compliance when it came to direct debits.

As the above table shows, one of the other four major banks had a compliance rate of 90 per cent, behind only three smaller banks who achieved 100 per cent compliance.

The report did praise the information available on the NAB website as it included information on the difference between a direct debit and a recurring payment and outlined the steps required to cancel a direct debit with the bank, including how to go about it online, in the branch or over the phone.

Have you ever had problems trying to cancel a direct debit arrangement with a bank? Have you been forced to contact the service provider to cancel a direct debit after being told by a bank that it was the correct way to cancel the arrangement? Why not share your thoughts in the comments section below?

If you enjoy our content, don’t keep it to yourself. Share our free eNews with your friends and encourage them to sign up.