{kind=link}

No-one knows how long they will live or how long their savings need to last. Yet an accurate estimate of life expectancy is crucial when planning for retirement.

A National Seniors survey found that older Australians underestimate their life expectancy by up to seven years and the financial services industry cannot necessarily be relied on for better estimates. Research by the Actuaries Institute into the methodologies used by both superannuation funds and financial advisers shows that many retirement planning tools may not always reflect best practice when it comes to determining and allowing for life expectancy.

Understanding life expectancy

In November 2020, the Australian Bureau of Statistics (ABS) released updated life expectancy data showing that life expectancy for a 65-year-old male in 2017-19 was 20 years and for a 65-year-old female 22.7 years. These are the average number of years that a 65-year-old could expect to live, assuming current age-specific death rates are experienced through his/her lifetime.

Read more: Why ageing populations are an asset

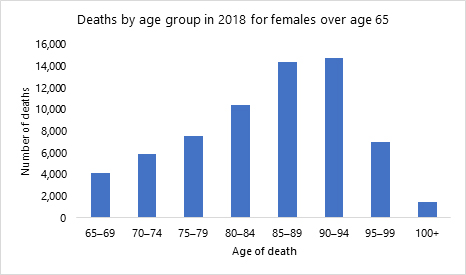

But averages do not tell the whole story. There is a wide range for how long different individuals live and the lifespan of each individual may well be very different to the average. The chart below shows the actual age of death for females who died in 2018 aged 65 or more.

These basic life expectancy numbers are not suitable for retirement planning. As an example, the ABS data tells us that life expectancy for a 65-year-old female was 22.7. That is, on average, a 65-year-old woman will live to nearly 88. However, the chart of actual deaths shows that 35 per cent of women aged 65 or more who died in 2018 were older than 89.

Life expectancy numbers are based on the whole population. It is crucial to consider mortality improvements along with socio-economic and health differences that might affect an individual’s life expectancy.

If a retiree uses basic life expectancy tables when planning for retirement, there is a good chance he or she will outlive their savings.

Retirement planning horizon

Your retirement planning horizon is the period over which you should be basing your retirement spending calculations. It will depend on your personal life expectancy, whether you are doing your retirement planning as part of a couple and your tolerance for longevity risk.

The reason you need to consider the age of both spouses is that joint life expectancy (the age of the second death) is longer than single life expectancy. Also, one spouse is typically younger than the other and can therefore be expected to dominate the required planning horizon.

Read more: How a marriage needs to adapt when a spouse retires

If you want to be confident that your retirement plan is robust, you might choose a retirement planning horizon that gives you, say, an 80 per cent chance that your savings will last as long as you live. For example, the Actuaries Institute paper refers to earlier estimates that a couple – a 65-year-old male and a 62-year-old female – might consider a 35-year retirement planning horizon to be 80 per cent confident their savings will last to the second death.

Lifespan calculators

There are several calculators that factor in some or all of the necessary items, one of the latest being the Optimum Pensions Lifespan Calculator. It is based on the latest Australian Life Tables and incorporates health data from one of the world’s largest reinsurers of longevity risk.

Rather than just showing population averages, the results can be personalised by considering health and lifestyle factors, and it allows for both members of a couple. The Lifespan Calculator also allows you to choose from three confidence levels to determine your retirement planning horizon – the age you should use when working on your retirement plan.

Are you basing your retirement planning on an accurate assessment of your longevity? Were you shocked to learn how long you might live? Share your thoughts in the comments section below.

Read more: Retirement income system fails this group

Stephen Huppert is head of engagement at Optimum Pensions.

If you enjoy our content, don’t keep it to yourself. Share our free eNews with your friends and encourage them to sign up.

Disclaimer: All content on YourLifeChoices website is of a general nature and has been prepared without taking into account your objectives, financial situation or needs. It has been prepared with due care but no guarantees are provided for the ongoing accuracy or relevance. Before making a decision based on this information, you should consider its appropriateness in regard to your own circumstances. You should seek professional advice from a financial planner, lawyer or tax agent in relation to any aspects that affect your financial and legal circumstances.