{kind=link}

Andrew Podger, Australian National University

There is a case for not proceeding with, or at least further deferring, the legislated increase in employers’ compulsory superannuation contributions from 9.5 per cent to 12 per cent.

But the Grattan Institute’s latest analysis, published in The Conversation and elsewhere, does not make this case.

Rather, it demonstrates extremely well a totally different problem with our retirement incomes system, and falsely ties it to our 9.5 per cent so-called “super guarantee”.

That problem is the pension assets test, tightened in 2017.

The problem is the pension assets test

For a significant group of middle income earners, Grattan finds that an increase in savings through the super guarantee would lead to a reduction in lifetime incomes.

But that is equally true of a voluntary increase in savings, in any form other than increased investment in the family home.

A better designed assets test, preferably through a merging of the income and assets tests, would ensure that increased savings boosted at least retirement incomes. It would ensure that we didn’t penalise thrift.

Whether we should attempt to compulsorily increase in savings through the super guarantee is an entirely separate issue.

Grattan is right to point out that any increase in the guarantee would come at the expense of increases in wages. It falsely accuses proponents of an increase of insisting this would not be the case.

Read more: Productivity Commission finds super a bad deal. And yes, it comes out of wages

Perhaps some proponents of an increase do believe employers would or should bear much of the cost, but that is not consistent with the history of the super guarantee, one of whose strengths has been the sustainability of its funding by not adding to the cost of labour or inflation.

Those super ‘tax breaks’ scarcely exist

Another annoying aspect of the Grattan piece is the continued presentation of superannuation tax arrangements as “tax breaks”.

It is true that a shift in payments from wages to superannuation savings does, at that point in time, reduce tax revenue because of the difference between the contributions tax (generally 15 per cent) and wage earners’ marginal tax rates (for most, at least 30 per cent).

But what is the appropriate tax on savings, particularly savings that cannot be accessed until age 60?

The convention internationally is to exempt from tax entirely contributions and the earnings they generate, but to tax in full the benefits as they are paid out. If we did this, we would be imposing a greater immediate cost on the budget which would presumably be an even greater “tax break”. In reality we would be providing an appropriate tax regime for those looking to spread their lifetime earnings, in the knowledge that tax would be paid at the time they took money out.

Read more: ‘Catch up’ super contributions: a tax break for rich (old men)

Work done a few years ago for the Committee for Sustainable Retirement Incomes concluded that, after the Turnbull government’s superannuation tax reforms, our regime of a limited but progressive tax on contributions and earnings and no tax on benefits, produced very similar results to the conventional approach at all income levels, although it is implemented the other way around.

It means that by international standards there isn’t a tax break.

Moreover, as Grattan has demonstrated with its analysis of lifetime incomes, the impact of superannuation on age pensions disadvantages many people precisely because it saves the budget money in the long term.

The goal ought to be a comfortable retirement…

What would really help is if Grattan articulated what it considers to be the objective of the retirement incomes system, and focused its analysis on whether increasing the super guarantee would or would not help to achieve that objective, and at what cost.

The objective surely ought to be that Australians have secure and adequate incomes at and through retirement. “Adequacy” here has two components:

– sufficient to ensure no aged person lives in poverty (the role of the age pension); and

– sufficient to maintain pre-retirement living standards (which the role of superannuation and other savings, with the age pension contributing for people on less than average incomes)

There are legitimate debates about how to determine “adequacy”, particularly the second component.

Read more: Frydenberg should call a no-holds-barred inquiry into superannuation, now, because Labor won’t

Grattan claimed last year not only that the current 9.5 per cent super guarantee would do the trick, but also that most current retirees (who have not accumulated anything like a lifetime of 9.5 per cent of compulsory super savings) already receive adequate retirement incomes.

I remain convinced this is an extreme view, not consistent with international practice or analysis.

…which might mean contributions of more than 12 per cent

For those not eligible for an age pension (likely to be at least 40 per cent of retirees into the future), maintaining pre-retirement living standards will require contributions of 15-20 per cent (18 per cent is the OECD average); for those eligible for some age pension, the contribution rate required will be lower but, even at typical earnings, would most likely be more than 12 per cent according to Committee for Sustainable Retirement Incomes analysis.

Whether such a contribution rate should be compulsory is a legitimate question.

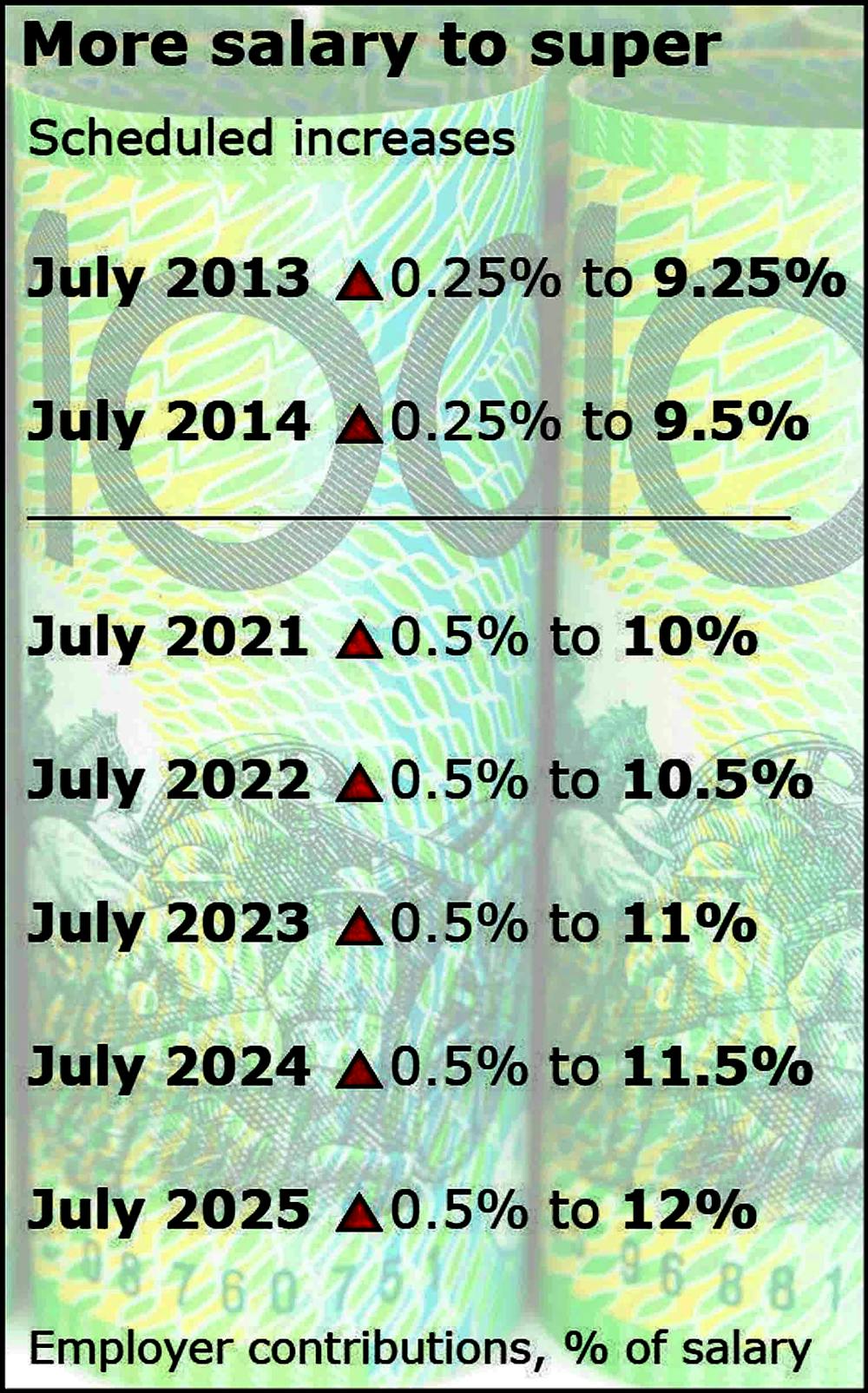

Perhaps the current low rate of wages growth warrants a longer deferral of the next legislated increase (though it will be seven years since the last set of two 0.25 per cent increases when the next increase of 0.5 per cent is due to come into force in 2021, and real wages will have increased by much more than this in the meantime).

Perhaps the burden on some young families of increasing compulsory savings would be more than their circumstances allow (although there are other ways of assisting them).

A concern I have, however, is that Grattan seems to suggest not only that the super guarantee not be increased beyond 9.5 per cent but that we would not then need to encourage most workers to voluntarily save more beyond that, including after their children grow older and become financially independent.

That seems to me short-sighted, and accepts a greater reliance on the age pension in the future than is desirable.![]()

Andrew Podger, Honorary Professor of Public Policy, Australian National University

This article is republished from The Conversation under a Creative Commons license. Read the original article.

If you enjoy our content, don’t keep it to yourself. Share our free eNews with your friends and encourage them to sign up.

Related articles:

What to do if you get a debt notice

Call to change rules for couples

Which assets test do I apply?