{kind=link}

Half a million people intend to retire within the next five years. However, it’s unlikely that anyone is truly prepared for what lies ahead.

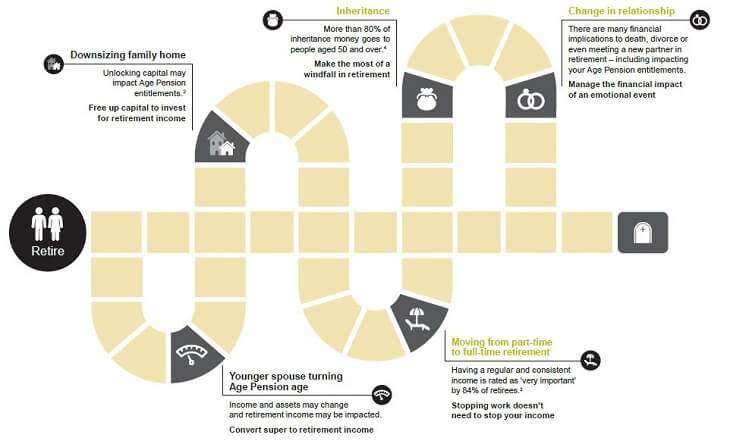

Life doesn’t always go to plan. Things change – markets can move the wrong way, relationships can break down, you may receive a sizeable inheritance or downsize your family home. Any change can have an emotional and financial impact, regardless of whether it’s planned or out of the blue.

In the second of a two-part series, we look at what to consider when moving from part-time to full-time retirement, receiving an inheritance and experiencing a change in relationship.

Moving from part-time to full-time retirement

Stopping work doesn’t need to stop your income.

There are a number of life changes that can impact retirement income – no longer receiving a pay cheque is a significant one.

For many people, retirement is when they stop commuting and clockwatching – and start to live a little. But the loss of a regular pay cheque can be disconcerting. Stopping work doesn’t mean you have to forgo a regular income.

Considerations

Chris is a 70-year-old homeowner, who is concerned about running out of money as he moves from part-time work to full-time retirement.

Before speaking to his financial adviser, he wonders if he should:

- rework his budget for retirement and cut back on all non-essential spending

- put his worries aside and invest in some high growth shares, optimistic that markets won’t be in a downturn when he needs the money

- revisit his retirement plan to ensure that his retirement income is sustainable and, where possible, his Age Pension entitlements are maximised.

Transitioning from work into retirement can be a big change financially. Contact your financial adviser to find out how an investment in a lifetime annuity can provide you with income for life.

Receiving an inheritance

Avoid any possible financial pitfalls of a windfall

There are a number of life changes that can impact your retirement income – receiving an inheritance is a common one.

Our desire for certainty is a deeply human trait, and the emotional challenges of retiring can exacerbate this need. Receiving a financial windfall could boost your retirement income, but an inheritance could also impact your Age Pension.

Considerations

Cameron is a 67-year-old homeowner with modest super and assets – until he receives a sizeable inheritance.

Before speaking to his financial adviser, he wonders if he should:

- spend some of the money renovating his house to hopefully increase the resale value

- put a chunk of money in a term deposit and the rest in a high interest savings account so it will be safe – even if it does impact his Age Pension

- revisit his retirement plan to take advantage of his increased retirement assets to build a sustainable lifetime income stream.

Even events like receiving an inheritance may upset the status quo. Contact your financial adviser to find out how a lifetime annuity could help you with income for life.

Change in relationship

Manage the financial impact of an emotional event

There are many financial implications to death, divorce or even meeting a new partner in retirement. Divorce or the death of a spouse can cause more than emotional grief for those in retirement – it can also drastically impact retirement income.

Considerations

Claire is a 70-year-old homeowner who is dealing with the loss of her spouse and concerned about managing her financial situation by herself.

Before speaking to her financial adviser, she wonders if she should:

- hold on to all current investments or sell them so she has one less thing to worry about – the financial world is a little daunting to her

- leave the account-based pension death benefit to just sit in the bank and wait until her grief paralysis passes – even though she’ll lose all her Centrelink benefits

- consider investments that could produce regular retirement income so she can rest assured she’ll have money to cover her essential expenses for life.

A relationship status change, even meeting a new partner later in life, may impact your retirement income. Contact your financial adviser to find out how an investment in a lifetime annuity can provide you with income for life.

Have you experienced one of these life-changing events? Did you seek advice to determine the best way forward? Why not share your experience in the comments section below?

Challenger is a preferred partner of YourLifeChoices.

If you enjoy our content, don’t keep it to yourself. Share our free eNews with your friends and encourage them to sign up.

2 Age Pension benefits will not apply to all individuals. Age Pension outcomes depend on an individual (or couple’s) personal circumstances and may change over time.

3 National Seniors Australia and Challenger, 2018, Once bitten twice shy: GFC concerns linger for Australian seniors, National Seniors, accessed April 2021, bit.ly/3cJPIQM

4 Danielle Wood and Kate Griffiths, 2019, Generation Gap: Ensuring a fair go for younger Australians, Grattan Institute, accessed April 2021, bit.ly/3xsHFQl

This information is provided by Challenger Life Company Limited ABN 44 072 486 938, AFSL 234670 (Challenger) and is current as at 26 May 2021. The information in this article is general only and has been prepared without taking into account any person’s objectives, financial situation or needs. Because of that, each person should, before acting on any such information, consider its appropriateness, having regard to their objectives, financial situation and needs. Scenarios, examples and comparisons shown are for illustrative purposes only. They should not be relied on by individuals when they make investment decisions. Each person should obtain and consider the relevant product’s Target Market Determination (TMD) and Product Disclosure Statement (PDS) before making a decision about whether to acquire or continue to hold the relevant product. A copy of the relevant product’s TMD and PDS can be obtained from your financial adviser, our Investor Services team on 13 35 66, or at www.challenger.com.au Challenger Life is not an authorised deposit-taking institution for the purpose of the Banking Act 1959 (Cth), and its obligations do not represent deposits or liabilities of an authorised deposit-taking institution in the Challenger Group (Challenger ADI) and no Challenger ADI provides a guarantee or otherwise provide assurance in respect of the obligations of Challenger Life. Accordingly, unless specified otherwise, the performance, the repayment of capital or any particular rate of return on your investments are not guaranteed by any Challenger ADI.