One of the big decisions as you approach retirement, or are knuckling down to plan for it, is setting an annual budget for when you do wave farewell to your working life.

There is no hard and fast rule about how much to spend in retirement. A lot will depend on your superannuation balance, your lifestyle expectations and your financial situation, but there are a few guidelines to help you plan and set a budget.

An easy rule of thumb to your spending expectations is to budget about 75-80 per cent of your annual working income.

This sum takes into account that in retirement you will no longer have work expenses such as commuting to work and a work wardrobe.

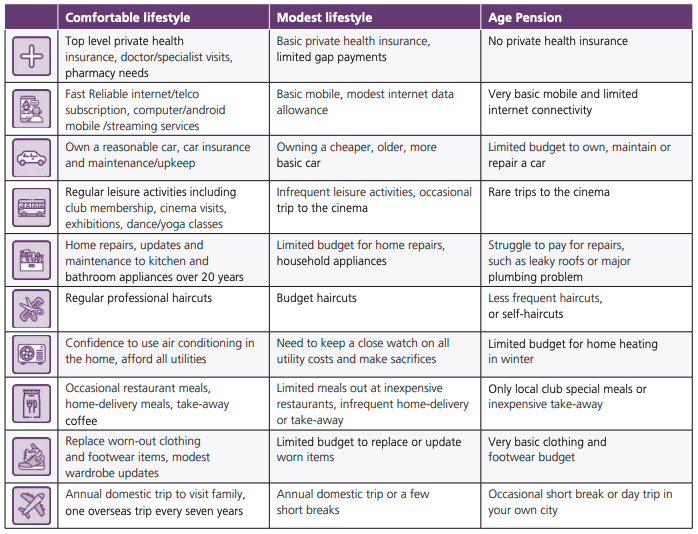

Comfortable vs modest

The Association of Superannuation Funds of Australia (ASFA) retirement standard provides annual expenditures required for comfortable and modest retirements called the Detailed Retirement Expenditure Breakdowns (DREB).

The DREB is updated quarterly to reflect changes in the CPI. It assumes retirees own their own home and are relatively healthy.

According to the ASFA, considering the latest CPI figures, couples aged 65-84 expecting a comfortable lifestyle should expect to spend about $71,723 a year, and singles $50,981 a year. For a modest lifestyle, couples should expect to spend $46,620.05 a year and singles $32,417 a year.

For those aged over 85, couples planning a comfortable lifestyle should budget $65,554 a year and singles $47,338 a year. Those on a modest lifestyle should budget about $43,000 a year for couples and $30,000 a year for singles.

According to the ASFA, the lump sum required for these spending expectations is $690,000 for a couple expecting a comfortable lifestyle and $595,000 for a single. The superannuation budget required for a modest retirement is $100,000 for couples and singles.

These figures assume that the retiree will draw down all their capital and receive a part Age Pension.

The following table shows how the ASFA weights its estimates:

Go your own way

These figures are just a guide, a good guide, but they will not fit all expectations.

Many retirees recognise that the early years of their retirement may be busier. They could perhaps continue to work part-time or choose to travel, both of which may become more difficult as they age.

“Often my clients might choose to spend a bit more in, say, the first five years of retirement,” said Antoinette Mullins, principal of Steps Financial told InDaily.

“You might want to have overseas holidays or buy a camper van and perhaps do some home renovations to make the house more liveable later in life,” Ms Mullins said.

It can be good to fit in as much as you can in the early part of your retirement, but be aware of approaching spending issues.

Often your health costs will increase. Australia has universal access to healthcare, but not all of it is free. A simple CT scan can cost $600.

And almost no-one likes to face up to the possibility of aged care, but the fact is costs are increasing, so it’s a good idea to plan early and explore your options.

A good – free – place to start your planning journey is the retirement planner calculator on the MoneySmart website.

It may also give peace of mind to consult a financial planner to map out your financial retirement journey.

Have you done a budget on your retirement spending? Did you go it alone or get some advice? Why not share your experience in the comments section below?

Also read: Is real estate the right asset to fund retirement?