One of the big decisions as you approach retirement, or are knuckling down to plan for it, is setting an annual budget for when you do wave farewell to your working life.

There is no hard and fast rule about how much to spend in retirement. A lot will depend on your superannuation balance, your lifestyle expectations and your financial situation, but there are a few guidelines to help you plan and set a budget.

An easy rule of thumb to your spending expectations is to budget about 75-80 per cent of your annual working income.

This sum takes into account that in retirement you will no longer have work expenses such as commuting to work and a work wardrobe.

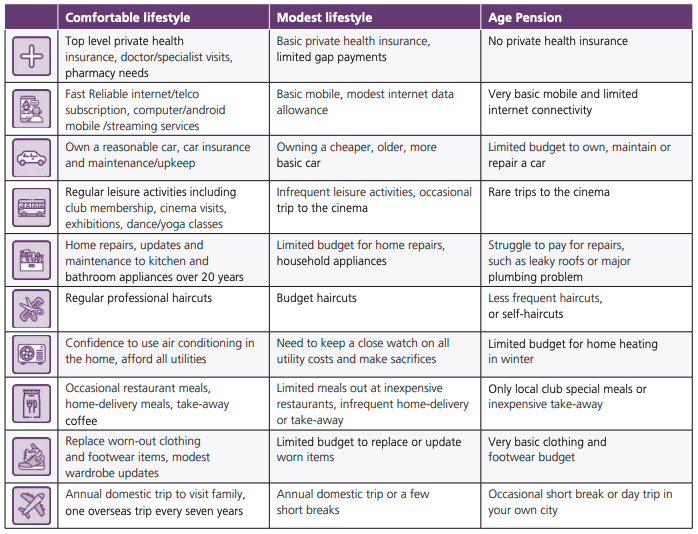

Comfortable vs modest

The Association of Superannuation Funds of Australia (ASFA) retirement standard provides annual expenditures required for comfortable and modest retirements called the Detailed Retirement Expenditure Breakdowns (DREB).

The DREB is updated quarterly to reflect changes in the CPI. It assumes retirees own their own home and are relatively healthy.

According to the ASFA, considering the latest CPI figures, couples aged 65-84 expecting a comfortable lifestyle should expect to spend about $71,723 a year, and singles $50,981 a year. For a modest lifestyle, couples should expect to spend $46,620.05 a year and singles $32,417 a year.

For those aged over 85, couples planning a comfortable lifestyle should budget $65,554 a year and singles $47,338 a year. Those on a modest lifestyle should budget about $43,000 a year for couples and $30,000 a year for singles.

According to the ASFA, the lump sum required for these spending expectations is $690,000 for a couple expecting a comfortable lifestyle and $595,000 for a single. The superannuation budget required for a modest retirement is $100,000 for couples and singles.

These figures assume that the retiree will draw down all their capital and receive a part Age Pension.

The following table shows how the ASFA weights its estimates:

Go your own way

These figures are just a guide, a good guide, but they will not fit all expectations.

Many retirees recognise that the early years of their retirement may be busier. They could perhaps continue to work part-time or choose to travel, both of which may become more difficult as they age.

“Often my clients might choose to spend a bit more in, say, the first five years of retirement,” said Antoinette Mullins, principal of Steps Financial told InDaily.

“You might want to have overseas holidays or buy a camper van and perhaps do some home renovations to make the house more liveable later in life,” Ms Mullins said.

It can be good to fit in as much as you can in the early part of your retirement, but be aware of approaching spending issues.

Often your health costs will increase. Australia has universal access to healthcare, but not all of it is free. A simple CT scan can cost $600.

And almost no-one likes to face up to the possibility of aged care, but the fact is costs are increasing, so it’s a good idea to plan early and explore your options.

A good – free – place to start your planning journey is the retirement planner calculator on the MoneySmart website.

It may also give peace of mind to consult a financial planner to map out your financial retirement journey.

Have you done a budget on your retirement spending? Did you go it alone or get some advice? Why not share your experience in the comments section below?

Also read: Is real estate the right asset to fund retirement?

{kind=link}

We are full pensioners and homeowners who are debt free.

1) Have never had private health insurance as it’s poor value for money. The public system here in FNQ has always provided excellent care including dental.

2) Have full mobile and top tier internet connection at home plus Foxtel, Netflix and Stan all in HD.

3) We have a top of the range diesel 4WD for comfort and for towing our boat etc.

4) We are not cinema goers but engage in some leisure activities, in my case tennis.

5) Our house is in good condition but whenever something does need repair I do it myself.

6) Have nearly always done our own hair, wife gets together with her friends and do each others.

7) Living in FNQ we have no reason to ever heat our house.

8) We mostly eat at home the same as always, but sometimes eat out at the club or elsewhere.

9) We have all the clothes we need which is not many in our climate.

10) We enjoy all the holiday breaks we want and use our pensioner long distance rail passes or fly or drive depending on the destination.

That is in response to the ten points in your article which in our situation is absolute nonsense.

Good on you David.

We are on part( 3/4) pension and can live quite comfortably , sure, not as well as we used to and you have to make lifestyle adjustments to compensate for the shrinking capital funds available.

Have to say though , looking through your 10 points ( including a new 4WD and a boat..!!) dont know how you do it. However not contrubition to the ever increasing private medical insurance really is a kicker along with living in FNQ .. as we have recently left that great part of the world and recolated to Sunshine Coast with consquent inceases in COL compared to FNQ.

Bakka, I did not say the car and boat are new, they are top models but are about ten years old.

Being quality and being looked after both probably have about another 15 to 20 years of service life left in them and as I am 74 I expect them to see me out.

That is the trick to an easy life as a pensioner I think, spend your money at around 65 setting yourself up with everything you need for what remains of your expected life. Own it all outright, look after it, retain a nest egg for contingencies, claim the full pension and make use of all the senior and pensioner concessions.

You will not have a luxury life style but you will have a very comfortable lifestyle.

And you know, even if you are unfortunate enough to need a nursing home one day the low cost public ones are the best choice as they are not being run by private operators who are only interested in your money not your care.

Lucky you.

It’s very difficult to generalise as everyone’s circumstances are different. Example. We rent and that costs $40grand a year. Find somewhere cheaper ? Haha. We are not alone. Many seniors still have mortgages outstanding. Others have family at home offsetting some of the costs. Fortunately at 76 I’m still working and receive a pension plus the work bonus, but there’s not many that are able to do that. Just saying.

“An easy rule of thumb to your spending expectations is to budget about 75-80 per cent of your annual working income.”

What happens when you do not get that much, how about 45%, with a Mortgage, Private Health, house hold upkeep etc, and a substantial debt due to Out of Pocket Expenses associated with 5 years of Cancer Treatment.

At least my Partner had the same Oncologist & Radiologist for all of her Cancer Treatment.

She lost her battle in Sept 2022.

I have also undergone treatment for Cancer, but I was lucky, they managed to remove all of it, and am currently on 6 month checkups.

We fit into the Comfortable Lifestyle category except for the overseas holidays.

We live on acreage with a very large house, which we maintain and update ourselves.

We have two vehicles, one new, one about 7 years old, serviced annually and fully insured.

It costs us $50K – $52K per year to live. We are fully self-funded – no part Age Pension.

What a lot of rubbish. As an 85 year old you get free medical, hospital, NDIS. Etc. You don’t go out for meals and prefer a microwave dinner to a takeaway meal. Someone comes to mow your lawn and clean your house. You would never even spend the fortnightly pension if you own your own home.

We are in our 70’s and on a full pension- own our own home, have health insurance, two cars, a caravan, interstate and business class overseas holidays every year.

Takeaway Tuesdays and a meal out every week. Buy clothes when we want if needed. We are in the “ sweet spot” by havin the maximum super before loosing any pension.

The difference is….. We don’t expect to have any money in the bank when we get to 85 . Just our home which will be warm and comfortable to put our feet up and bask in our wonderful life.

Few 85 year olds get NDIS, Lindtay. You have to have been under 65 when it was rolled out in your area to qualify. And medical and hospital is free for those with certain conditions, but many conditions and medications are not covered by the free system – or the wait times or conditions of free treatment make it unviable. Most of us only get 5 specialist visits a year covered by Medicare and even those are often not fully covered. We are lucky to have an excellent doctor who bulk bills, but many can’t access a bulk-billed GP who delivers acceptable quality service. I certainly can’t afford household help or anyone to mow my lawn and I don’t know how anyone gets that help free – but certainly the majority do not.

Then there are those who are paying rent or still have a mortgage, and they are really struggling.

I am living very comfortably now, but I have to plan for future high costs for dental work and optical. And I have to budget for household help and help with the yard in years to come, because I won’t be able to manage it as I age. For sure the aged pension won’t stretch to pay for a cleaner or gardener.

I don’t think it’s fair to assume that your situation is typical, much less universal. We should have some compassion for folk who are struggling. And it’s not fair to assume that their struggle is due to extravagance or trying to retain money in the bank (which they may well need for some specific purpose after age 85).

I don’t necessarily agree with the figures quoted by ASFA, but circumstances differ and generalizing is offensive to many. We should be supporting those whose needs are not being adequately met – not dismissing them.