As an investor your aim is to make money, which happens when markets rise. So naturally it’s tempting to try to time your entry point to ‘buy low and sell high’.

The problem with that strategy is that nobody really knows where markets are headed next. Australian shares have returned around 10.9 per cent per year over the past 100 years but those returns aren’t spread out evenly.

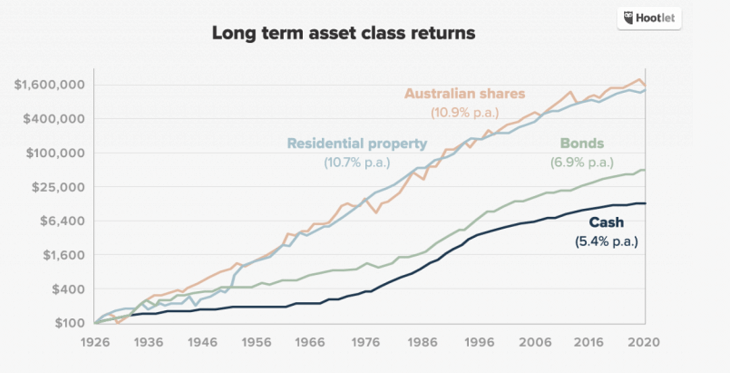

ASX market returns

Over short periods of time, like a week or a month, it’s actually a flip of a coin whether markets will be up or down. Short-term movements in markets are random ‘noise’ around the long-term uptrend.

You can ignore the professional fund managers and TV commentators too. Most of them get their market timing calls wrong. This is one reason 80 per cent of them do worse than simply buying and holding the Australian share market index and doing nothing.

When is the right time to invest?

If you wait for prices to fall to grab a bargain, you’ll need to get two decisions right – when to be out and when to get back in. That’s easier said than done.

Read: Could ‘buying the dip’ boost your retirement income?

Even when markets do fall, if you wait too long to buy back in, you’ll miss out on returns as they go back up. Then if you’re completely out of the market, you have no way to benefit from the gradual increase in share prices over time.

Thankfully, there is a way you can avoid the anxiety of investing everything at once. It’s a simple investment strategy called dollar cost averaging.

The best time to invest is… regularly

Dollar cost averaging is one of the most powerful ways to get ahead when you invest. Instead of waiting for the ASX to fall to time your next investment, dollar-cost averaging is a strategy to invest your money gradually over a few weeks or months.

If you invest small amounts regularly over a period of time, you’ll buy your investments at an average price over time. That way you get to take advantage of any market dips (and pay a lower price) or gains if markets rise.

Procrastination is the enemy of investment returns

Trying to time the market is fraught with psychological barriers. When markets fall and it seems like everyone is abandoning the investment ship, it’s extremely difficult to pile in. That’s why most people who wait on the sidelines for the next market correction end up waiting too long and missing out all the way back up.

Read: Mistakes to avoid when share markets fall

Take December 2018 as an example. The S&P ASX/200 (Australian share market) had fallen 15 per cent in three months and most people were sitting on their hands. Fast forward six months and the share market was up 20 per cent from its December lows.

Those who held off from investing in December 2018 because of either: a) fears of further market falls or b) hope of even cheaper prices, missed out on dividends and capital growth.

On the other hand, in September 2020, the market had risen 11 months in a row and it might have been tempting to wait on the sidelines.

If you wait to save up large lump sums to invest you potentially risk:

- missing out on compound returns while you wait

- being more impacted by short-term market movements once you’re invested.

Ultimately, if you have a long-term investment mindset, dollar cost averaging can reduce anxiety about losing money while you invest. Even if markets don’t dip, you’ll end up buying as markets rise and be making a profit on your earlier purchases.

How do you dollar cost average?

A dollar cost averaging investment strategy is easy. Simply make a plan of how much you want to invest and set up a regular top-up. The easiest way to do that is by setting up an automatic transfer from your bank account. Sarah King, head of client care and advice at Stockpot, wrote this guide on how to dollar cost average.

Checklist before you start investing

We believe you should only consider investing once you have:

- 3-6 months’ worth of expenses saved as a ‘rainy day fund’

- a minimum of $2000 to invest. It could be from savings, a bonus or tax return

- a time horizon of at least three-plus years to give you the best chance of great results.

Do you consider yourself a confident investor on the share market? What’s your advice to others who have their L-plates on? Why not share your thoughts in the comments section below?

This article has been republished with permission.

If you enjoy our content, don’t keep it to yourself. Share our free eNews with your friends and encourage them to sign up.

Disclaimer: All content on YourLifeChoices website is of a general nature and has been prepared without taking into account your objectives, financial situation or needs. It has been prepared with due care but no guarantees are provided for the ongoing accuracy or relevance. Before making a decision based on this information, you should consider its appropriateness in regard to your own circumstances. You should seek professional advice from a financial planner, lawyer or tax agent in relation to any aspects that affect your financial and legal circumstances.

{kind=link}