{kind=link}

Millions of Australians are headed for a second rate retirement because they’re in a poor performing super fund, according to a report that names the best and worst funds.

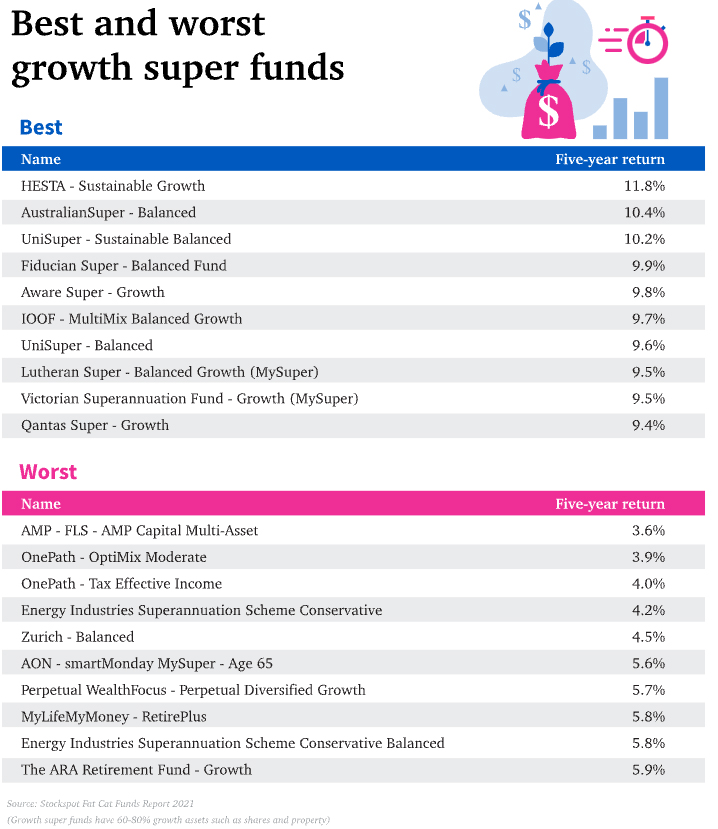

Stockspot’s annual Fat Cat Funds Report, now in its ninth year, analyses and compares about 600 investment options offered by Australia’s biggest 100 funds – and names names.

A key warning in its analysis this year relates to the number of funds charging unreasonable fees – boosting the nation’s annual $30 billion spend on super fees.

The report says that $7 billion of Australians’ superannuation is sitting in the worst 40 Fat Cat Funds, which have fees above 1 per cent.

Chris Brycki, author of the report and CEO of Stockspot, says people must ensure their fees are below 1 per cent. “I can’t stress the importance of this enough. Currently there are almost twice as many high-fee funds (more than 1 per cent p.a. in fees) than low fee funds (less than 1 per cent p.a. in fees),” he says.

READ: Will your super fund still be in business in five years?

A super fund investment option is classified as a ‘Fat Cat Fund’ if it is in the bottom 10 performing super funds within a particular risk group, such as balanced, growth and so on, over five years. Conversely, a ‘Fit Cat Fund’ is in the top 10 performing super funds within a particular risk group over five years.

The worst fund this year was OnePath, which had 10 Fat Cat Funds. In second place was AMP (six Fat Cat Funds), followed by MLC, Zurich and Energy Industries Superannuation Scheme (three Fat Cat Funds each). They hold $7 billion of your super, according to the report, and charge more than $120 million in fees every year at an average of 1.8 per cent. That would equate to an average lifetime loss of $200,000 due to fees and poor performance by retirement age, the report says.

The best Fit Cat Funds are Unisuper and Qantas Super, with four Fit Cat Funds each that returned 20 per cent more over five years than the Fat Cat Funds. In joint second place were Australian Super and Fiducian Super, followed by third place-getters IOOF, Aware Super, AMG Super, and Holden Employees Superannuation Fund.

READ: Concessions help wealthiest Australians avoid tax with super

The top three Fit Cat Funds all charge less than 1 per cent in fees per year.

The Your Future Your Super comparison tool, which compares MySuper products and took effect from 1 July, ranks 80 MySuper funds. But there are millions of super accounts outside that line-up.

Mr Brycki says the YourSuper tool is a “great starting point” for researching the best funds, but is not comprehensive enough and doesn’t help to identify the best performers for each level of investment risk.

“This is because MySuper funds vary greatly in the amount of investment risk they carry for members,” he says, “so comparing MySuper funds without adjusting for risk levels is not useful.”

Mr Brycki contends “there’s an obvious lack of information from government bodies”.

“When clients first start investing, they naturally become more interested in their largest investment – their super. When this clicks, it’s impossible not to want to research and make sure you’re taking the right actions.

“While consumers should definitely be looking at performance and fees, they need to make sure they’re taking into account the risk level of each fund. Remember, for every stage of life, there will be a different risk profile and investing strategy.”

READ: Unlucky for some: 13 worst super funds

He says you should be comparing funds that have the same risk levels, rather than just focusing on the best performers, which might have much higher risk levels than lower performing funds.

“Some high performing funds have 98 per cent growth assets,” he says, “while a lower performing fund might have 75 per cent growth assets.”

Key takeaways:

- Poor fund performance is largely due to high fees – never pay more than 1 per cent p.a. in fees.

- Funds often expose members to higher risk and lower returns by overcomplicating their investment strategy, i.e. not indexing.

- The two factors with the best predictive power are the risk profile – the mix of growth assets such as shares and property versus defensive assets such as bonds and cash –and low fees.

Find Stockspot’s full list of best and worst performing super funds here.

Do you find it difficult to compare funds and different investment levels? Do you pay more than 1 per cent in fees? Why not share your experience in the comments section below?

If you enjoy our content, don’t keep it to yourself. Share our free eNews with your friends and encourage them to sign up.