{kind=link}

For many Australians, superannuation is their biggest investment besides their home, but it’s an area with typically low levels of understanding and engagement.

It’s not surprising that younger members, decades away from retirement, are not overly interested in super, since receipt of their pot of funds is well into the future. But it becomes front of mind for retirees and those approaching retirement, as accessing those funds becomes a tangible reality.

Accumulation and pension

There are two phases in superannuation, with phase one being the accumulation phase. This is what most people are familiar with when thinking of superannuation, with their employer making regular payments into their super account.

The second is the pension phase. This is when you start to use the money that has been built up by transferring some, or all, of your funds into a pension product to access a regular income stream.

When reaching preservation age – the age at which you can access your superannuation – you can choose to withdraw your super all at once by receiving a lump sum payment or you can divvy up the payment into instalments and receive it over time using a retirement income product such as an account-based pension. Your preservation age is determined by your date of birth, as shown in the table below, based on details from the ATO website.

Preservation age

| Date of birth | Preservation age |

| Before 1 July 1960 | 55 |

| 1 July 1960 – 30 June 1961 | 56 |

| 1 July 1961 – 30 June 1962 | 57 |

| 1 July 1962 – 30 June 1963 | 58 |

| 1 July 1963 – 30 June 1964 | 59 |

| From 1 July 1964 | 60 |

Once you reach preservation age, you are able to access your super, though you are not required to make any withdrawals from your accumulation account, even if you are retired. Some individuals may choose to keep their super in an accumulation account (the account into which their employer made payments) if they don’t need a regular income from their super, if they’re still working or plan to work in the future or if they wish to retain their insurance cover held through their superannuation.

Further, for the lucky Australians who have more than $1.7 million in their account, the ‘transfer balance cap’ limits the amount that can be transferred into a pension account. This is a limit on the amount of super that can be transferred into the pension phase, which applies over your lifetime. Since 1 July 2021, the limit is $1.7 million; before 1 July 2021, a cap of $1.6 million applied to all individuals.

Lump sum vs account-based pension

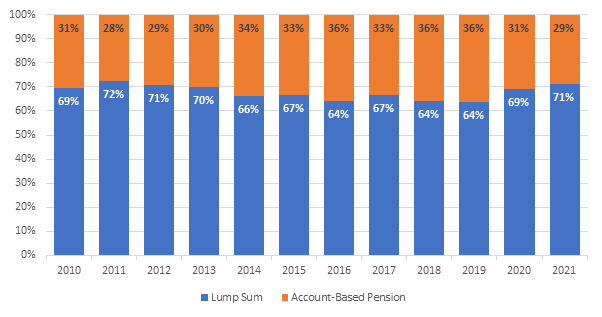

The majority of Australians reach preservation age and withdraw their super as a lump sum payment. The chart below shows that, since 2010, there hasn’t been much change in the percentage of Australians who prefer a lump sum withdrawal from their retirement nest egg at retirement age. In 2021, 71 per cent of people withdrew their super instead of starting an account-based pension, with 29 per cent selecting the latter option.

Proportion of benefit payments paid

Reasons for this behaviour include using it to pay off outstanding debt such as a mortgage, to assist family members, renovate, buy a new car, make other purchases that were not previously affordable or invest for retirement. Some also withdraw their super and simply put it in a bank account for ease of access. However, with interest rates at all-time lows for an extended period, there are minimal returns. Further, some people may not be aware there are other options.

Account-based pensions

For individuals who do not opt to withdraw a lump sum, an alternative is to transfer funds into an account-based pension product or ‘allocated pension’. This is an account where your superannuation funds are invested and from which you receive a regular payment that provides an income subject to minimum drawdown requirements.

An account-based pension provides a stream of payments to live on, which can help you to budget your spending. Your account balance is also able to be invested in a range of investment options offered by your fund.

The pension payments will be made until your balance reaches zero, so it does not provide a guaranteed income for life. The payments are also counted as income for the purposes of the income and assets tests that form the eligibility assessment for the Age Pension.

Minimum drawdown rates

Retirees who have started a pension are required to ‘draw down’ – i.e. reduce their pension account balance by a certain percentage set by the government.

In March 2020, because share markets were being hit hard by the pandemic, the government announced that retirees could reduce the minimum drawdown rate.

| Age at 1 July of each year | Temporary drawdown rate to 30 June 2023 | Standard drawdown rate from 1 July 2023 |

| Preservation age to 64 | 2% | 4% |

| 65 to 74 | 2.5% | 5% |

| 75 to 79 | 3% | 6% |

| 80 to 84 | 3.5% | 7% |

| 85 to 89 | 4.5% | 9% |

| 90 to 94 | 5.5% | 11% |

| 95 and over | 7% | 14% |

How are your pension funds invested?

You can choose how the funds in your pension account are invested based on the options offered by your super fund. You should always check the level of growth assets (such as Australian and international shares) before making a decision, as the higher the level of growth assets the more ups and downs you’re likely to experience. It is also important to look at the level of growth assets and not just the name of the investment option, as there isn’t a standard approach to naming investment options across funds.

The majority of pension accounts are invested in Capital Stable, Conservative Balanced and Balanced options.

Capital Stable options include more defensive assets such as bonds and cash and have 20 to 40 per cent invested in growth assets. Conservative Balanced options have 41 to 59 per cent invested in growth assets while Balanced options have 60 to 76 per cent invested in these assets.

The table below provides a summary of performance for Balanced options based on pension products, to provide an indication of the range in performance outcomes across the market as at 28 February 2022.

Pension return benchmarks – Balanced options (%)

| 1 year | 3 years | 5 years | 7 years | 10 years | |

| Top quartile | 10.0 | 8.7 | 8.8 | 7.9 | 9.9 |

| Median | 8.8 | 8.1 | 8.2 | 7.3 | 9.4 |

| Bottom quartile | 8.0 | 7.6 | 7.6 | 6.5 | 8.8 |

* Returns are net of investment fees, tax and implicit asset-based administration fees. Annualised returns for each period are shown.

The top quartile indicates the top 25 per cent of funds outperformed this figure, while the bottom quartile is the cut-off for the bottom 25 per cent of performers. The median represents funds that sit in the middle between highest and lowest in terms of performance. The table above shows the range in performance across the market, with the best-performing Balanced options delivering returns of 9.9 per cent or more per annum over 10 years, compared to 8.8 per cent or less per annum for the lower 25 per cent of funds in the market.

The table below provides a summary of performance for Capital Stable options based on pension products.

Pension return benchmarks – Capital Stable options (%)

| 1 year | 3 years | 5 years | 7 years | 10 years | |

| Top quartile | 4.9 | 4.7 | 5.0 | 4.9 | 6.2 |

| Median | 4.2 | 4.3 | 4.7 | 4.4 | 5.6 |

| Bottom quartile | 3.1 | 3.8 | 4.1 | 3.7 | 5.2 |

* Returns are net of investment fees, tax and implicit asset-based administration fees. Annualised returns for each period are shown.

The table above shows the range in performance across the market, with the best-performing Capital Stable options delivering returns of 6.2 per cent or more per annum over 10 years, compared to 5.2 per cent or less per annum for the lower 25 per cent of funds in the market.

Pension account fees

In addition to investment performance, the fees charged by your fund are also important in determining the lifestyle you’re able to lead. A helpful rule of thumb is to check how much your fees are as a proportion of your account balance. If the fees are more than 1 per cent of your balance, it’s worth seeking advice and investigating available options.

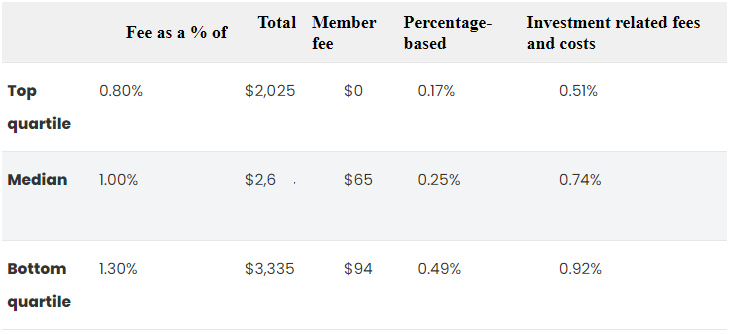

The table below summarises fee benchmarks for Balanced options across the main pension products in the market, using an account balance of $250,000. The top quartile indicates the cheapest funds, the bottom quartile is the cut-off for the more expensive funds, and the median represents funds that sit between cheap and expensive in terms of fees. There is a considerable range in fees charged by funds across the market, with the most expensive 25 per cent of funds charging $3335 or more, compared to $2025 or less for the cheapest 25 per cent of funds.

Pension fees on a $250K account balance – Balanced options

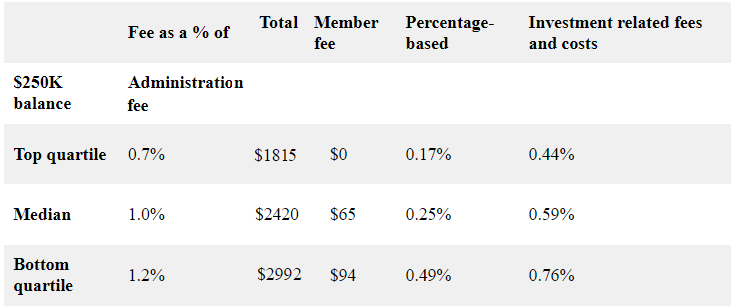

The table below summarises fee benchmarks for Capital Stable options across the main pension products in the market, using an account balance of $250,000. For these options, the most expensive 25 per cent of funds charge $2992 or more, compared to $1815 or less for the least expensive 25 per cent of funds in the market.

Pension fees on a $250K account balance – Capital Stable options

Retirement Income Covenant

The government’s Retirement Income Covenant legislation passed in late 2021 and outlines how funds should go about developing effective retirement income strategies to support members in and approaching retirement. It encompasses key things funds should consider in terms of the types of products and advice services for members.

Funds are required to have a retirement income strategy publicly available on their websites by July 2022. Funds are not required to develop or offer new retirement income products at this stage. However, they need to consider whether they should make any changes to existing product offerings.

Funds’ retirement income strategies may also include the types of tools and information they make available to support members in achieving their retirement goals (e.g. budgeting and expenditure calculators, education on topics related to retirement and projections of potential retirement income levels achievable).

In addition to account-based pensions, some funds may develop annuity-style retirement income products. The main difference to an account-based pension is that these types of products will provide an income stream for life.

Products such as QSuper’s Lifetime Pension product provides an income stream for the remainder of your life. If you pass away, your beneficiaries can access any balance of funds invested in the product instead of this going to the remaining pool of people in the product, as per a standard annuity type product.

Expect to see more funds introduce retirement income products of this nature, as they progress their retirement income strategies.

Financial advice

Given the importance of your superannuation investment and the complexity of the transition from accumulation to retirement, including tax implications, we suggest contacting your super fund to find out what advice services are available to you.

The government’s MoneySmart website offers information on how to select a financial adviser.

Camille Schmidt is market insights manager at SuperRatings. She has a PhD in finance from Macquarie University.

Disclaimer: All content in the Retirement Affordability Index™ is of a general nature and has been prepared without taking into account your objectives, financial situation or needs. It has been prepared with due care but no guarantees are provided for the ongoing accuracy or relevance. Before making a decision based on this information, you should consider its appropriateness in regard to your own circumstances. You should seek professional advice from a financial planner, lawyer or tax agent in relation to any aspects that affect your financial and legal circumstances.

Is it any wonder that people don’t take an account based pension! The charges are over the top expensive considering the products on offer along with the investment options are not particularly geared towards older people. I realise that our superannuation system is only just beginning to really mature but the complexities around pension and super in this country are just hideous. I really feel for those whose English skills may be a bit limited because there is so much information that one needs to know. As for financial advisors, I read ‘Banking Bad’ by Adele Ferguson – what any eye opener. Makes me very cynical (in case you hadn’t noticed) about the system generally.