Peter Martin, Crawford School of Public Policy, Australian National University

Want to keep working after you’ve reached pension age?

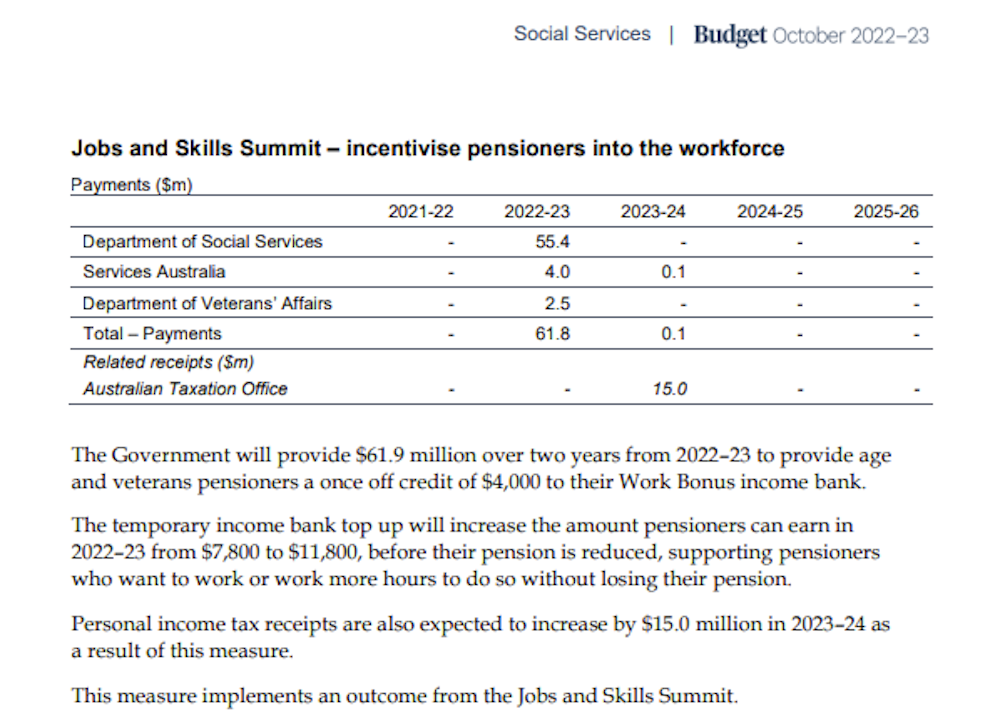

The Australian government has just made it a little bit easier, increasing the amount you can earn per year from work before losing some of your pension by $4000 on an ongoing basis.

Late last year, it temporarily upped the so-called work bonus from $7800 per year to $11,800 to “incentivise pensioners into the workforce”. It was part of the government’s response to its September jobs and skills summit.

{kind=link}

It meant pensioners could earn an underwhelming $227 per week from work without harming their pension, up from the previous $150.

The rules for older workers are very different in New Zealand. In fact, if Australia adopted New Zealand’s approach, we could have an extra 500,000 willing workers – a fair chunk of them paying tax.

What’s NZ doing differently for older workers?

Last month, as part of his employment white paper, Australian Treasurer Jim Chalmers made the increase to $227 per week permanent.

Dr Chalmers headlined the announcement: Getting more Australians back into work.

But it’s doing an underwhelming job. In Australia, 15.1 per cent of the population aged 65 and older are in some kind of paid work, up from 14.7 per cent a year earlier.

In contrast, in New Zealand the proportion has just hit 26 per cent. That’s right – more than one-quarter of New Zealanders aged 65 and older are employed.

It’s a similar story if we look at how Australia and New Zealand compared to others internationally on labour force participation (which covers those in paid work plus people actively looking for it).

New Zealand wants to see that number rise further. It has been talking about 33.1 per cent of its population aged 65 or more in paid work, which is what Iceland has.

What is New Zealand doing for over-65s that Australia is not?

You won’t find it mentioned in either Treasury’s employment white paper (released in September) or the Intergenerational Report (released in August) – even though National Seniors Australia pointed it out in submissions.

One crucial thing New Zealand is not doing is annoying pensioners who work.

Australian pensioners in paid work get called in for discussions with Centrelink if it looks as if they are at risk of doing too many hours and going over the $227 per week limit.

The more you work, the more your pension is cut

Pensioners who do go over the $227 per week limit lose half of every extra dollar they earn in a cut to their pension.

Plus tax, this means they lose a total of 69 per cent of what they earn over the limit where their tax rate is 19 per cent, and 82.5 per cent on the portion of earnings taxed at 32.5 per cent.

And this is after the boost designed to “incentivise pensioners into the workforce”.

Last year’s jobs summit also set up a Women’s Economic Equality Taskforce. It reported this week, drawing attention to the “disincentive rates” facing second earners (usually women) who return to work after caring for children.

It said that taking the loss of benefits, tax and childcare costs together, the penalty for returning to work was more than half of what was earned on the first three days of the week, and up to 110 per cent of what was earned on the fourth and fifth days.

My point here is that the losses facing age pensioners who attempt to work are of a similar order – in Australia but not in New Zealand.

Australia’s rules aren’t just stopping pensioners from taking on extra hours. They seem to stop them taking up paid work at all.

There were 2.6 million Australians on the Age Pension in June this year. Only 83,925 reported income from working. That’s just 3.2 per cent.

NZ pensioners keep their pensions

What’s different about New Zealand is that New Zealand’s pensioners don’t face a penalty if they work. They simply face income tax.

In New Zealand, the age pension (which is called superannuation, making it confusing for Australians) is paid to everyone of pension age. There’s no income test or assets test. You get it because you are a citizen or permanent resident.

Australia wouldn’t need to go as far as New Zealand to get the same benefit. We would simply need to ditch the pension income test in cases where that income came from paid work, leaving the assets test in place.

Then there would be no concern about working.

Half a million reasons for change

If we made that change – and if the same proportion of older Australians chose to work as New Zealanders – we would soon have an extra half a million older Australians able to step into fields such as teaching, where there are 15,500 vacancies, and healthcare and social assistance, where there are 68,100 vacancies.

It would cost the federal government money because it would put more Australians of pension age on the pension.

But it would cost less if we abolished the special tax concession for seniors and pensioners, known as the seniors and pensioners tax offset. In New Zealand, senior citizens face the same tax rates as everyone else.

And it would cost less as more pensioners earned wages and paid income tax.

Calculations prepared for National Seniors Australia by Deloitte suggest that beyond a certain point, the change would become revenue positive – actually boosting federal coffers – as the extra income tax revenue outweighed the cost of the extra pensions.

National Seniors is calling its campaign ‘Let Pensioners Work’.

Tapping into the cash economy

Importantly – and here’s where we get to a fact National Seniors might not like me mentioning – that would happen not only because more senior Australians were employed, but also because more senior Australians were employed legitimately.

It’s hard to get a handle on how many senior Australians are working and being paid in cash, which they store rather than bank to avoid tripping the income test. But we do know this.

At the end of March, there were 18 Australian $100 notes in circulation for each Australian resident, an astonishingly high proportion given the use of cash for transactions is collapsing.

In New Zealand at the end of March, there were just five New Zealand $100 notes in circulation for each New Zealand resident.

That may be just a coincidence.

But New Zealand is certainly making it easier for retirees to work legitimately, rather than stay at home or accept cash in hand.

Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University

This article is republished from The Conversation under a Creative Commons licence. Read the original article.

Would you be more inclined to work if Australia had a similar set-up to that in New Zealand? Share your thoughts in the comments section below.

Also read: Age pensioners to benefit from changes outlined in government white paper

{kind=link}

I have been going on about this for years. It’s very frustrating to be involved in work that, while benefiting my finances and helping employers who are desperate for workers, I lose 50 cents in the dollar. I’m not asking for an increase in the pension. Just simply allow me to retain what I work so hard for. Pretty simple really😉

I totally agree. It’s high time the Australian government stopped being so downright greedy.

Sounds fine as long as any changes do not penalise those who, for whatever reason, either don’t want to work or can’t work.

I would be willing to work if I was permitted to keep my pension as well as my earnings. I would not mind paying tax on my earnings, but I object to having my pension added to my earnings for taxation purposes, which is what is done here at the present time.

If the government is being paid tax for earnings, the pension should be tax-free. Because the pension on its own, without earnings, is below the present tax-free threshold. But our greedy politicians insist on over-taxing and therefore the present condition remains status-quo.

The current Australian concept of incentivising by way of penalising needs to be done away with. When this occurs, life will be so much more pleasant in this country.

No, I don’t earn income outside my pension, which makes existence very difficult in our present economic climate, in case you were wondering.

Yes all very nice guys BUT isnt the age pension in NZ much lower than ours in Oz,?

Maybe the really need to work to get a living income.

No, not really. The total package including concessions is about equal. However I agree that both Aged Pensions have fallen short of the target of a livable income.

NZ is smarter because the Aged Pension is below the taxable threshold, but any taxable income earned, is taxed. This provides more incentive to work if you want a little extra.

Because the IRD (NZ Tax Office) is already in place, Work & Income (NZ equivalent of Centrelink) needs fewer staff per thousand people to manage their Aged Pension System. This allows the NZ Government to be more generous with concessions.

If you are a self funded retiree then the Austn system is better than NZ system. In Aust.your pension is tax free. In NZ, yes you get the gvt pension as well, but both amounts are combined & then taxed.

Not true. Self-funded retirees in Australia pay tax the same as all other Australians, paying tax on any taxable income in excess of $21,500 and this tax is based on the marginal tax rates that apply as income thresholds increase.

It probably helps that politicians in NZ are on the same pension system as all other New Zealanders. As such they have a fairer system.

Everybody, regardless of their assets gets an aged pension (called NZ Superannuation). If you want to earn more to top up your pension, you can and many do. Like any earner, you pay progressively higher levels of tax depending on how much you earn.

NZ Super is payed just below the tax-free income threshold, so unless the recipient has other income, is a simple zero-tax return. Even a nominal amount of money in savings does not push NZ Aged Pensioners over the threshold.

Our process here with deeming and all the other complexities is anything but simple.

There are not thousands of NZ government employees micro-managing the NZ aged pension; just the IRD who ensure every NZer earning income pays the appropriate tax.

Australia has more government employees per aged pensioner that the NZ Super system. The NZ system costs less per superannuant to provide, but actually provides more. Aged NZ people actually get NZ Super at 65. Australians often have to wait longer before they are eligible.

In Australia, the way pensioners lose 50c in the dollar on earnings above $227 per week, only tells half of the story. People then pay additional tax on their earnings, so can end up losing between 69% and 82.5% depending on the tax bracket they fall into. And most then need to pay the Medicare levy. Why would any sane Australian even consider working in the Australian scheme?